In the mordern trend, people needs better but instant things without wasting any extra time or extra money. That’s were instant products like packet fries and cup noodles were introduced.

At that moment a company named venky’s came up with instant products mix at a lot cheaper rate. Even this products had so much in demand that they were found in all the malls and departmental stores.

Being a workholic myself i prefered losing the least amount of time. Wasting time to prepare dishes wasn’t a thing i was looking forward. That’s when i got to know about this product mixes and i thought of buying one to trying it. Arriving at the outlet i took some packets of idle mix, some french fries and some packets of meat balls. Surprisingly it cost me way lesser than the ones provided in fast food centers. Coming back home, i tried preparing a packet of idle and i was amazed it took me max to max 30 mins. To be really honest guys it tastes better than the ones made at home. Even it was way better than the ones found in outlets costing me more than 200-250 bucks. I was really satisfied.

Having a curiosity, i looked behind the packet for the manufacturer where it was written venky’s india limited. Further with my curiosity into play, i checked the manufacturer in money control if it was listed or not. Surprisingly it was, that’s when i went through its financials, operating laws, profits and losses and everything, but it was coting below average.

According to us we the investors shouldn’t really fall for the financials ‘cause most of the financials are provided to manipulate the traders. That’s the reason i focused more into its product demands, sales and stability. Going into more details and doing a bit of market research by myself i further found that customers of venky’s are regular. Corporate people are the high rated customers who actually buys such instant product mix in bulk and stores them for regular and future use, not only them but also this are the favorites of childrens which increases a lot of sales for the company and the only reason is they are way cheaper, tastes good and takes some minutes to cook. So, as we all have the idea when the demand reaches to its peak the sales starts climbing the ladder and that’s when the company enjoys there profits. With rise in sales increases the amout of profitibility which eventually effects its stock price in the near future. And basically, this was the only reason i went for venky’s india limited.

I bought venky’s shares when its price was 394.04rs per share. Now i can show you how my strategy worked. Traders can see the rise in the price of venky’s, which is has touched rs 4725 per share gaining a huge profitibility.

With the alteration of attire in the recent years people are falling for unique trends and styles but in a cheaper price with superior quality. But irrespective of demands well-known companies started rising the rates for their own purpose. That’s where I came across DONEAR.

A story comes across this. Days back being a teenager I was fond of modern attires and sticking to the trends. But the rise in price was the only barrier. So one day while going through market with one of my uncle who is also a cloth merchant in Bura bazaar, while I came across prices way over middle class people can afford, I noticed a brand having its advertisement all over the market place showing prices people actually crave for, that was DONEAR. Normally prices of well-known companies don’t stand below 700-800Rs and more there DONEAR kept its prices below within 25%(approx.). Cost effective amazing quality with latest trends made me think, you see guys there’s no end to middle class family who would love to afford such good standard products at a cheaper rate.

Having a curiosity, I went for its details firstly asking my uncle about the brand who gave a pretty much good response about it. Lately coming back home I started my own research about this brand and by god’s grace I found it in money control list coting at 15.77Rs. Observing share price in this rate made me purchase it then and there. Further I recommended my clients and their families to purchase this for I believed this one was a multibagger in near future. Lately you guys can notice that this was indeed a stock to be purchased for this stock rose silently up and still going.

I purchased DONEAR when the price was 15.77Rs with my own strategy and an expectation, where none of them failed me rather made me gain a profit for you can see that DONEAR have touched a height of Rs 89.50. With a hope for more hike in price per stock in the near future. We do not have any freshly entries right now but people who already have this share owned should definitely hold it for higher gains in the near future.

After a huge loss by Kingfisher Airlines the aviation sector was observed with a negative sentiment by the market. Despite being observed as a negative sentiment India is a growing economy and soon it will be touching 3trillion economy. Once India touches this landmark travel and transport sector will have a bigger role to play.

In the 21st century people have lesser time and lot to provide so wasting a single minute can cost huge. Being a workaholic myself I would always prefer to waste the least amount of time. As per my work I also had to travel and guys honestly train journeys are time consuming. For instance, once I had an emergency, so I had to travelling from Calcutta to Delhi. I took a train which took approx. 18 to 19 hrs. but via flight it minimizes the time and destination can be acquired within 2 to 3hrs. In this fast-paced world where every other individual is in a hurry to fulfill their needs and wants, to create an identity, to showcase their talents and these are only possible with accurate time management. So, wasting these precious times only for travelling can affect their growth right…!?

Lately as I did a bit of research over this thing, I discovered during the year 2015-16 the crude oil prices were rising vigorously which ultimately made the prices of aviation go high and stocks went easily down. Moreover, aviation companies at that point of time didn’t had an economy type seats, all were premium classed, thus the rates were pretty high which caused 60% of seat go empty. In this period SpiceJet which came up with astonishing cheaper rate for travelling but despite having cheaper rates the company faced some internal affairs, something regarding ownership of SpiceJet between Malan Brothers and Ajay Singh which eventually affected the company’s p/l account. Further due to such internal issues the stock prices were pretty down that’s when I purchased its stock with an expectation that it will rise soon after the internal affairs resolves.

The time I purchased stock of SpiceJet it coted at Rs22.93. Later we can observe that in the year 2017-18 the stock price rose up till 156.3Rs per share and we’re still positive with share. While it is making a W formation in the chart, we can expect a positive rise soon or later.

In the recent times, people are getting addicted to online markets. Buying product in cheap and by comparing with variety other without any hassle with quick delivery have made online market come in trend. People expected more and more innovative products and that’s where Sasta Sundar came up with an excellent innovative idea about selling medicine and medical goods online.

As I started my research, I learnt, back during 2016 Calcutta had no online medical goods seller. That’s when Sasta Sundar entered the market with its huge client base due to their previous business firm. Though during 2015-16 there were some companies that took up this online market of selling medical goods, but the cost was same as the retailers and none had any exciting discount to attract a large number of customers. In order to go into detail of my research I purchased medicinal goods both from Sasta sundar as well as its rival companies. Truly speaking guys, others were providing products with prices same as the retailers, Sasta Sundar provided me with exciting discounts with a lot cheaper rate. Not only that the delivery and packing were far better than the rest. Moreover guys, it was the only company listed with stock market, which gave it an advantage to rise above its competitors.

So, Introducing Sasta Sundar with such an innovative idea of providing medicine and medical goods within 48 hours in cheaper rate with 30% above discount, people started to get the craze for this company. Further medical goods needed for personal or private use can easily be bought without any hassle or uneasiness. Especially for women, they have a lot uneasiness while buying ladies products and moreover they are not so comfortable, that’s where this company started gaining the lime light among its customers. With wide range of delivering area all over the country including Calcutta Sasta Sundar took a stand for itself. Even the company’s operating profit and balance sheet looked too really very strong.

Keeping in mind all these reasons, it made me purchase shares of Sasta Sundar when it was coting at Rs67.33, with my strategies in hand. Lately our things have been proved within 2years, when it went double than it was till Rs 152.95 and trust me, it has the potential to rise more.

In the recent years, consuming liquor is in trend. Get togethers, family functions, parties, disc every place has an option for hard drinks and liquors for, it maintains a class. Moreover, all my near and dear ones also were fond of consuming liquors occasionally.

So, it was one time in an official party I was invented where there was this huge bar. Honestly guys to maintain a standard I had to consume a little. While having a drink I observed varieties of vodka bottle had a single manufacturer. I took a bottle, checked it. That’s when I encountered with this brand Radico Khaitan.

Returning home and with my curiosity into play, I started my research upon this company. Going through its website I observed that the website was quite strong with a pretty good valuation all over. Moreover guys, I figured out that overall sales in this sector will never go down rather rise even when government applies strict guidelines over it. Moreover, doctors themselves are in support of consuming alcohol for health issue at a limited volume though, but this reason has triggered the sales for products like this.

Going into more detail in my research I literally got attracted to this share for at that moment Radico Khaitan was going at Rs90 and the market valuation at that moment was 1k crore. If compared to their competitors like the united spirits had a market valuation near about 25k crores or if we talk about united breweries, they had a market valuation of 40-50k crores. So Radico Khaitan was available at a cheaper rate at compared to its competitors. More importantly when there was a positive upward movement among all other brands and companies Radico Khaitan didn’t move a place, so I went more into details where I noticed and observed as well that the management of this company, the owner everything was at a positive ground. There was nothing negative that can shook its customers. Being the leading manufacturer of Vodka I discovered all the high graded places consist of Radico Khaitan products and not only that middle-class families could also afford it to buy. Being the leader in Vodka production it acquired 20-30% market share of Vodka in the stocks, besides the dividend structure was pretty attractive for all the investors. Further they started introducing newly made and exciting products to attract the teenagers which actually triggered their sales a lot.

So basically, all the above-mentioned reasons provoked me to purchase share of Radico Khaitan because basically consumption of alcohol in the recent future will increase rapidly. Thus, increase in demand will obviously increase the amount of sales which is directly linked up with the company’s profitability and hence the share price will start feeling the effects.

The time I purchased Radico Khaitan it was coting at Rs 371.98 which eventually rose up to Rs 499 gaining me a huge profit. We have a hope that it can have an upward rise till Rs 1200. Fresh entries are restricted as it has already gone up approx. 4 to 5 times from its buying price, but it is really an excellent share for long term investors.

Well you see, according to me “the power of accurate observation and a little reasoning can lead to an upsurge.”

Every time I walk out of my house, I state to observe every little change in the products and brands, there value, amount, price, increase or decrease in demands, etc. So, it was this one time I was walking down the streets of Dalhousie I noticed a lot of advertisement of this company Manappuram Finance. A full-fledged advertisement with all types of promotion were up which actually fascinated me a lot.

This advertisement made me interested and a lot curious about Manappuram Finance. So, I thought of going through this company. You see, living in Calcutta I noticed there were a lot of branches of Manappuram Finance all over providing gold loans rapidly as compared to the local banks. Local banks do provide gold loans, but they do have a lot of terms and conditions which are a lot complicated for general people. I myself have faced a lot of hassle to receive a small amount of gold loan. At that place, Manappuram Finance provided all sorts of easy transactions that to rapidly taking max to max 20minutes.

“Our products aim at delivering value to the customer. No matter what his economic status is, we believe that time is precious, and everyone is entitled to courtesy and prompt service with high levels of transparency” the following was quoted by an employee of Manappuram. For this exquisitely smart service by Manappuram Finance, the company is highly appreciated by its customers and general people all over which eventually increase the demand for its service. Naturally increase in demand tends to increase in sales with ultimately results in the upsurge of its stock price.

Basically, I bought shares of Manappuram Finance for the above reasons hoping for a better return. Purchasing Manappuram Finance when it coted at Rs 27.06 with my strategies in hand, gave an awesome return when it touched the top at Rs 130.45

According to my perspective I guess India bulls Ventures was the biggest multibagger I came across my career. I remembered investing an amount of Rs30000 whose return was approximately 7lakh 50thousand that made me go awestruck within just a couple of years which eventually means the return percentage is around 3000%. It takes years and years to make 10 times extra returns from the amount invested, then there’s Indiabulls Ventures the biggest multibagger I ever encountered with, took me to heights in just a couple of years.

According to a lot of famous investors, one should not really invest only in one segment. So, keeping that in mind I went searching for a stock in the financial segment. Finally, I got introduced too Indiabulls Ventures. With time I started my research about this company and came up with a lot of material.

Indiabulls Housing Finance was the flagship company for Indiabulls Ventures. In 2016 when actually I purchased the stock of Indiabulls Ventures, the company owner of Indiabulls Mr. Sameer Gehlaut made the performance of all the companies pretty well. If we take Indiabulls Ventures or Indiabulls Housing Finance or even if we take Indiabulls Real estate all had a top-notch performance all round. Lately, I even found out that companies like Soril Infra and even Soril Holdings were also a part of this huge firm Indiabulls.

In 2016 just after May, there was a sudden fluctuation of the stock price starting from Indiabulls Housing finance whose impact would definitely affect Indiabulls Ventures directly or indirectly. Moreover, Indiabulls were into a monstrous project of constructing a luxurious resident in Mumbai with bridges and other facilities beyond people expectation, not only that Indiabulls ventures were trying to cover consumer and retail loan segment. So basically, with all this in the hands of Indiabulls Ventures, the valuation of the company would increase by 2-3 times. Lately checking their balance sheet and profit and loss statement which you can find in my research reports we had generated, everything was going admirably great.

So, all the reasons provided above made me believe that this was going to be something bigger and better than expected. Not only Indiabulls Ventures but also Indiabulls Housing Finance even Indiabulls Real Estate, Soril infra, Soril Holdings, I have bought like anything and I have made money like never before. Till now for me, this is the biggest multibagger ever found in my career. It has crossed Rs 800, though it has a downward fall now, we expect a hike till Rs 1200 to Rs 1500 in near to short term.

DMart is a chain of hypermarkets in India founded by Radhakrishna Damani in the year 2002. As of October 2018, it had 160 stores across India in the states of Maharashtra, Andhra Pradesh, Telangana, Gujarat, Madhya Pradesh, Chhattisgarh, Rajasthan, National Capital Region, Tamil nadu, Punjab, Karnataka . DMart is promoted by Avenue Supermarts Ltd. (ASL). The company has its headquarters in Mumbai

In the recent times, DMart has become way to famous among its customers and has recently been listed in the stock market.

I came across DMart back in 2017 when I went for an official tour of 5days till Madhya Pradesh. I literally had no idea about anything back there. So one day I went out to purchase some personal stuff of mine, but I didn’t get a proper shop. After a little laundering here and there, I came across this mini big bazaar called DMart. To my utter surprise it was a shop cum mall. Variety of products and with cheaper rate.

You see, according to my vision, it was a smaller concept than its competitors like the big shopping malls and it is easily accessible to all standards of people without any hassle. Moreover, to buy petty household stuff and groceries one prefers small stores than going into malls. That’s where DMart played a significant role by introducing itself all over the country, in each locality so that people can easily access their products and goods with comfort. As the products are easily accessible, the sale rating will obviously leap up soon.

While being easily accessible to all standards of people, I came across products under its own brand name. Purchasing some of their products to try, those had a pretty good quality at a cheaper rate. Further going on to their sites I noticed DMart have introduced online purchasing of all types of groceries with online payment and also cash on delivery available for more comfortable way to purchase.

Thus, all this above-mentioned reason, I expected that soon there will be a hike in the sales of DMart thus increasing the profitability of the company which will finally create a good position in the stock market. So, we have invested on DMart in 2017 when it was coting at Rs 641.70 which later leaped up till 1428.80Rs.

In 2015-16 software business was very progressive during that period. Lots of companies took interest over this sector for better opportunity to earn that’s where I across with FSL share.

FSL as in Firstsource Solution Limited was typically owned by the best business group Sanjeev Goenka Group and soon it started to take over the software market for we all have a clear idea that Goenka group or the RPG group have the best business mentality for its business progress. All we know CSC which the flagship company of their brand is and not only that they have also started business with spencer and other brands so we can estimate that FSL will perform in near to short term. Till date it isn’t performing like it should, its rate is hovering around 35-40Rs but in the near to short term we can expect that it can have a bounce back of 50 to 60% in the rates right after the elections.

Determining the above reason, I purchased this share when it was coting at Rs 37.95 which later leaped up till 43.05Rs gaining me Rs2040. We can expect a hike in the rates of this share sooner right after the elections.

In the late 2016, there was a lot of competition between the banks. Lots of new offer and policies were launched, huge amount of loans outflowed. Where most of the banks focused on high levelled corporates and MNC’s in that place HDFC not only focused in the high-level corporates but also had that same focus upon the middle-class families. That’s when my attention fell over HDFC Bank Shares.

I myself is a customer of HDFC bank so I actually felt everything which ‘m gonna explain you guys. I actually noticed while comparing with other banks HDFC had an easy access to loans like if we want credit cards or consumer loans its was easily accessible as compared to its competitors, not only that the rate of interest was very limited with which made an impact on me with all other customers and clients. Further doing my own research I observed that year by year their loan book was increasing and no new NPA’s were not appearing. As I went more deeper into detail, I got to know all other big banks were more concentrating upon big and high levelled corporates whereas HDFC bank was more into retail more and middle-class families. What they were doing was, as they were concentrating more upon middle class families, they provided loans amounting to Rs 40000-50000 where the chances for becoming an NPA had a lower rate as compared to big corporates as the chances of becoming an NPA had a higher rate.

You see, according to my analyses there is a greater risk in providing high amount of loan to big corporates than providing smaller amount to the middle-class families. The problem stands her, providing loans to bigger corporates will amount more than 1crore. Whereas providing loans amounting to Rs 50000 to 1lac or a little above from that 1crore the risk for being an NPA is lessen. HOW? You see if a big corporate becomes an NPA then the big amount can be a Bad Debt but even if 20 middle class customers owing 1lac each becomes NPA only 20lac becomes bad debt leaving behind 4crore 98lac safe and secured.

This were the reason I opt to purchase this share when it was coting at Rs 1005.36 which later leaped up till 2157Rs and I am still very bullish for the share but as it is a large cap stock no fortune can be build but for a constant return we can definitely hold on to its shares.

As we all know midcap and small cap stock are the ones that made people rich, over large cap stock. This share has the biggest gains as compared to large cap stock. Thus, I went for Sanwaria.

Sanwaria Consumer Limited, A FMCG Food Processing company of the Sanwaria Group was incorporated in April 1991, by Lt. Shri Ram Narayan Agrawal and commenced its operations in 1993. It is one of the largest integrated food processors in India and is engaged in the business of manufacturing and selling of Rice, edible oil and staple food products like Pulses, Sugar, Soya Chunks, Wheat Flour, Rice Flour, Salt, Suji, Maida, Besan, Daliya, Soya Meal etc.

During the period of 2016-17 there was a discussion going all over that Sanwaria would tie up with Patanjali products. Lately Sanwaria Consumer entered into an agreement with Patanjali Ayurved to manufacture and supply Soya Chunks or Soya Bari in the Patanjali Brand.

Though the Company had been supplying chakki fresh Atta to Patanjali in the past, the Board expects more such agreement in the near future looking to long association of the Sanwaria group with Patanjali and of promoters with Hon’ble Baba Ramdev for its other products like Soya bean Oil, Rice Bran Oil and Basmati Rice etc.

Looking to the recent tie-up of Patanjali with online platforms or virtual marketing networks like Flipkart, Amazon, Bigbasket, Grofers etc. SCL Products will also be available on all these platforms as a manufacturer. Further looking to leadership position of Patanjali in FMCG sector of India, The Board of Directors is confident of the favourable impact on the overall top line and bottom-line growth of the Company due to the association with Patanjali in the coming quarters.

Nowadays people have became more and more secure about all types of edible products such as rice, pulses, wheat, salt, Suji, Maida, Besan, even mixes like poha, that’s the reason people demands more and more safe and healthy products rather than loose flour or rice, etc. Here SCL played its part, they started offering secure and healthy products with attracting packages at a cheaper price. Moreover, the quality of goods provided were trusted by almost all the customer as per my market research. Soon demands started leaping up. SCL also then started its online platform and home delivery option open for its customers which soon become an advantage with a variety of goods and with trusted quality at a cheaper rate and option open for home delivery there was a high inflow of demand which eventually started the increase in their sales.

All this reason provoked me to purchase shares of SCL when it was actually coting at Rs 3.61. At that time, it was a very good buy and we can hold it to acquire a higher target within the next couple of years.

Nowadays each and every building, agricultural sector needs a conventional way to extract and inflow of water. That’s where the need of pumps arises. There were a lot of companies who introduced themselves in this sector but among them came up Shakti Pumps, producing some of the best quality pumps throughout India.

While I went for an outing in the outskirts of India. I noticed people are using only one brands pump, Shakti pump. As I asked them the reason the only thing they said was, that is the most trusted among all others. Further I did a small analysis where I found out that India’s leading manufacturer of energy efficient submersible pumps, Shakti Pump was well-known in the industry. They create products for several sectors including agricultural, industrial, domestic and horticultural. Shakti Pumps provides a range of solutions in many areas with its array of world class, cost & energy efficient pumps.

According to me, what I think is, In the recent times, where a lot of o flats and building coming up demands for a conventional way to extract water started hiking up. Being the most energy efficient pump manufacturer Shakti Pumps started to make an identity for themselves. With time Shakti Pumps started manufacturing more and more variety of pumps which even include solar pumps, submersible pump, pressure boosters and so on for variety of uses. Not only the quality was superior but also the price was so affordable that making a name for themselves wasn’t a big game to play. Moreover, they had a massive reach all over south India which played a crucial role. Further checking its balance sheet and P/L account I found it very viable and clear.

While Shakti pump was coting at Rs140.12 I purchased this share which later leaped up and crossed 750 in 2018, and we still have a prospective that shakti pump will hike up till 1200 -1500 in near to short term.

The 21st century have become a modernistic age with people more in freshly brewed trends and styles. The more time passes by more people are attracted to fashionable goods and products such as watches, jewelleries, etc. and to be honest when it comes to watches the brand TITAN comes up from everyone.

The watches division comprises of brands The watches division comprises of brands Fastrack, Sonata, Raga, Octane and Xylys. I literally had a super craze for watches and to be really honest guys I never left this brand. Look at its research I provided, In 2011, the company secured, licence for marketing & distribution of Tommy Hilfiger and Hugo Boss watches. Favre Leu be was incorporated in 2012. In 2018, the division accounted for ₹2,126 Cr in revenue which was 10% of the total of the company. Titan being the largest in India and is synonymous with the category. It caters to men, women and children across the length and breadth of the country. As you know, It also has a sub-brand Raga is a very popular women’s brand in India. Its distinct design language has captured the hearts of women across India. Titan also caters to the premium men’s watch market with an extensive range of watches. The razor-thin Edge series and the light-fuelled HTSE collections are just some of the timepieces that hold their own in Titan’s wide portfolio. In India, the category is present in the organized and unorganized sector, which makes it difficult to estimate the annual market size of the category in India.

According to most of the people TITAN means watches but there are several other brands under TITAN which works for different products. The 2nd most renowned product sold by TITAN are jewelries, TANISHQ. When I went to a TANISHQ store I literally was awestruck. The store was in a superb condition with the people were so great and people were literally crazy to purchase more exciting designs and stones, etc. Again, TANISHQ introduced some exciting offers to attract its customer, which was given by none. Coming to my research part, Xerxes Desai started the brand TANISHQ in 1995. Zoya was launched in the luxury segment, while Mia, a sub-brand was under TANISHQ for work-wear jewellery. TITAN’s jeweler sales fetched ₹13,036 crore. In 2016, Titan invested in CARATLANE who reported a turnover of ₹290 crore in FY 2017-18. TANISHQ by June 2014, TANISHQ had 167 retail stores nationwide, and announced the opening of 30 more by the end of 2015. In May 2015, TANISHQ enrolled Deepika Padukone to be the brand’s ambassador. In 2017, TANISHQ launched a sub-brand called RIVAAH targeting the wedding segment. In January 2017, the Titan group merged its Gold Plus stores with the larger TANISHQ retail brand. In April 2017, TANISHQ launched the sub-brand MIRAYAH to cater to women under their 40’s. December 2017, TANISHQ launched the AVEER LINE, its first line of products for men.

TANISHQ has already rose to a newer height but with introduction of raw diamonds the demands and sales can cross the expectation of the company. Moreover, all high standard and rich people are more into diamond business because they think diamond as an investment, which will increase the sale as well as the profitability.

While both TITAN watches and the jewellery brands having a top-notch profitability in the market TITAN also had its hand over optical. TITAN EYEPLUS, the eyewear business from Titan Company, was launched in March 2007. Being a guy with specs I understand the problem as well I know the solutions for it. All people wearing specs want a durable but at a lower price rate, similarly the design should be attractive and not only that its used be user friendly. And to be honest TITAN EYE WEAR was a brand that literally provided every little demand expected by its customers. Coming to the business ground, the move was an initiative to redefine the industry and straddle the marketplace with quality standards, unparalleled in India’s prescription eyewear industry. Benchmarked against the best in the world, Titan Eye plus herald’s standardization in the eyewear industry. Following Tata ‘s principles of quality and trust, the brand offers international quality standards enhanced by practices such as transparency in pricing, contemporary design and styling in the highly fragmented and undifferentiated Indian optical retail segment. Titan Eye plus has over 470 exclusive stores operating in over 200 cities and offers a wide range of stylish and contemporary eyewear. Titan’s Eyewear business recorded an income of Rs. 415 crores in 2017-18.

TITAN didn’t really stop here. Two more brands of TITAN, SKINN a brand for perfume and TANEIRA a brand for sarees were also introduced by TITAN. Which recorded a sale Rs.95 crores, a growth of 45.9% in 2017-18.

Designed in-house and created by six world renowned Master Perfumers including Harry Fremont, Michel Girard, Fabrice Pellegrini, Nadege Le Garlantezec and the celebrated Alberto Morillas and Olivier Pescheux, these French-made perfumes are international interpretation of HIM and HER. The array of fragrances portrays a young woman’s sensuality in SKINN IMERA; her warm seduction in SKINN NUDE and her charms and complexities in SKINN CELESTE. SKINN EXTREME celebrates the sporty vitality of a man whilst SKINN RAW defines masculinity and SKINN STEELE is a power trip of complex spices. The current portfolio of SKINN includes these 6 exciting variants in the EDP (Eau De Parfum) format and are crafted to last longer with notes that endure and grow pronounced with time.

Titan took a step forward in the saree division. Taneira, being the youngest brand of Titan Company Limited was conceived during an internal crowd sourcing of ideas around 2015. Multiple teams suggested sarees as a product category and rigorous rounds of evaluation finally resulted in sarees as the winner for a pilot project. Sarees was a natural extension of Titan’s value proposition. In ethnic wear, the saree is perhaps the most common traditional Indian dress for women and has a market of Rs 37,837 crore(approx.) so even if TANEIRA grabs 10 to 15% of the market it would rise to a new height.

Basically, going through my own research, I provoked myself to purchase TITAN shares. In 2015 I purchased TITAN when it was coting at Rs 351.15 which rose up to 1035.25Rs in 2017-18.

With India being a developing country techniques and methodologies are also changing with time. Starting from industrial sector till agricultural sector every method and techniques are getting advanced and getting promoted. Especially the agricultural sector has drastically started changing from old methodologies to newer techniques and methods. To support our agricultural sector ESCORT GROUP has taken a step forward.

From breaking fresh ground for Indian Infrastructure to nurturing the earth with harvests of prosperity – From mobilizing the economy on the rail-tracks of progress to be its driving force on the highways of the nation – Escort group are transforming lives, with the power of technology and imagination. Introduction of newer tractors Equipped with modern engineering and machines with extreme power and traction. Farmtrac is a tractor that remains ahead of its time. This premium range of tractors is available in the range of 37 HP to 75 HP and is known for pulling bigger traction with greater efficiency. It is a high performance, versatile, rugged machine with maximum comfort for the driver. Farmtrac series of tractors present a potent combination of style with substance. Further, the pioneer of farm mechanization in India, Escorts Agri Machinery has in the last seven decades, committed itself to enhancing India’s agricultural productivity and add value to the farmer’s life. Escorts currently provides technologically superior range of 12 HP to 80 HP tractors. With a growing network of over 800 customer touch-points, Escorts Agri Machinery ensures the satisfaction of its customer base of over 14,00,000 and also promises maximum uptime of their tractors and equipment.

Escort group didn’t stop at the agro sector but also took a step forward to Infrastructure development in India. It is a challenge transformed into opportunity, by ESCORT GROUP. The goal was not merely nation-building; it is to create conditions for maximization of national economic strength, which carries deep into the growth graphs of future. Today, ESCORT provide equipment for material handling, road building, earth moving and other services, addressing the large national opportunity with a comprehensive basket of products. In doing so, they help meet the growing requirements of the country’s infrastructure development, mining, realty, and other sectors. Think of a material handling operation, and Escorts has a crane for it. Their cranes range from 10T to 40T, with varying reach on different axes. Their material handling machines are safe, economical and highly productive, capable of lifting and placing loads and also traveling long distances. As a result, they not only make the operator’s job easier, but also ensure that he is able to deliver more in less time.

ESCORT GROUP even took up projects of providing railway equipment. Escort’s Railway Equipment Division (RED) possesses a rich, multi-decade experience in the Manufacturing of critical railway components. The division (operationalised in 1962) is one of the oldest such units in the country, partnering the Indian Railways in its modernization journey. The division is a market leader across all its product offerings. RED develops cutting-edge technology products in a state-of-the-art research and design facility and through collaboration with leading technology providers. The division has specialized in the safety, comfort and reliability niche. Escorts has ultra-modern, precision manufacturing facilities for Distributor Valves and is the largest manufacturer in Asia, having supplied over 100,000 nos. to Indian Railway for various freight and passenger car applications.

Taking all the above-mentioned information into account I opted to purchase its stock when it was coating at Rs 134.56 which eventually took a leap and crossed 900Rs. Right now, the rate is 655.70Rs and I believe it will rise up again in near to short term.

Most of the people doesn’t really question upon the products of tata. The brand name itself provokes customer to purchase products of tata. Maximum people rely on the products of tata. Tata Global Beverages Limited (formerly Tata Tea Limited) is an Indian multinational non-alcoholic beverages company headquartered in Kolkata, West Bengal, India and a subsidiary of the Tata Group. It is the world’s second-largest manufacturer and distributor of tea and a major producer of coffee.

Coming to its products, the packaged drinking water of tata is, my personal favorite, HIMALAYAN marketed by NourishCo, a joint venture between Tata Global Beverages and PepsiCo India. Himalayan is bottled in Dhaula Kuan, Himachal Pradesh, and available in 200 ml, 500 ml, 750 ml, 1 litre and 1.5 litre bottles. Himalayan is the only natural mineral water in India to be awarded international certification by Institut De Fresenius, Germany — the world leader in the treatment of environment pollution and production technology of natural mineral water. It has granted Himalayan the highest grade for a water company. Secondly, TATA WATER PLUS, developed in collaboration with international scientists and Indian nutrition experts, Tata Water Plus represents the larger mission of NourishCo Beverages. Tata Water Plus is available in 1 litre bottles and 200 ml pouches. A litre of this wonder drink meets 40% RDA for copper and 30% for zinc. And finally, TATA GLUCO PLUS An affordable on-the-go re-hydration solution, Tata Gluco Plus comes packed with great taste and instant energy. Tata Gluco Plus has been brought to the Indian market through NourishCo Beverages, our joint venture with PepsiCo India. NourishCo focusses on delivering ‘Healthy Beverages for a Healthier India’ and intends to enhance the hydration category in the country.

The costing of these product lies max to max 20Rs which is later sold at a price more than Rs50. Making a good amount of profit.

In the recent time people have become more and more health efficient and thus they opt for better health products. I myself became a lot health conscious and I started preferring Green tea. Nowadays as recommended by doctors Consuming Green tea is more into course. Even here I came across a Tata Global product who launched one of its brands in the name of TETLEY which became the biggest-selling tea brand in Canada and the second-biggest-selling in United Kingdom and United States. Further tata global also got more of its products there is Tata Tea the biggest-selling tea brand in India and JEMČA which is the biggest-selling tea brand in Czech Republic, tea pigs, good earth are some more successful products introduced by the tata global.

Tata global didn’t really stop themselves in packaged water or production of tea, they always have coffee brands which is similarly successful like the others. Eight o’clock, Grand Coffee, Map Coffee are the coffee products introduced by tata.

Further to expand their territory Tata global In 2012, Tata Global Beverages ventured into the Indian cafe market in a 50/50 joint venture with Coffee Company. The coffee shops branded as “Starbucks Coffee – A Tata Alliance” source coffee beans from Tata Coffee, a subsidiary company of Tata Global Beverages. More and more outlets were presented by them in all the states of India which increased a lot of their sales.

So, observing all the points above mentioned I started investing in tata global beverages when it was coting at Rs 90 which literally went up till Rs 328.1 and I believe that it will obviously touch the amount of Rs 500-600 in the near to short term.

In this modern era, fashion is the biggest trend trending all over the world. Fashion is ever-evolving creators will be sensitive, agile and open to the rapidly evolving fashion market. Creation exceptional brands and experiences that reflect the various identities and aspirations of Indian consumers is the main motive for all the manufacturer. Almost all the company in this sector wants to be the leading lifestyle fashion company in India by creating exceptional brands and shopping experiences that will bring alive the Indian idiom of fashion.

Like all other companies Future Group was also a company who joined this sector. It was this one day during the famous Durga puja in Calcutta I went for shopping. Going from one mall to another, I checked through their prices which was way over for any middle-class family, till I came across brand factor. A well-known and established mall. Going in I was amazed to check out their rates. They seemed so affordable for almost all middle-class families, as compared to mall like the Pantaloons or shopper stop. I previously have heard a lot about Brand factory but visiting and checking out myself made a clear idea for me. As we know customers are more attracted to cheaper rates and quality and eventually variety of designs and styles. And to be honest guys brand factory provided its customers with every single thing that they crave for.

Coming back home with my curiosity into play I started finding brand factor’s parent company, and I came across FUTURE LIFESTYLE FASHION. Hence, I started doing a little bit of research about them. I came across a lot of stuff. Let me share.

What future group did was they introduced brand factory in the most common areas alongside of big bazaar (a future retail). Further they started purchasing in a huge quantity like if pantaloons purchased 1000 quantity brand factory purchased 10000 or more that’s where they were more preferable to get more discounts. More over they purchased six to eight month’s old designed costumes which lowered the actual price because the brands can clear there closing stocks. That’s the reason how they provide at such a cheap rate. Further to attract customers they started providing exciting discounts and brand-new offers.

If I seriously start comparing with other malls the rates and amount of discount are so much user friendly for all classed people. And to be honest visiting myself personally I was very much impressed. Where shopper stop and pantaloons are providing a shirt in Rs 2000 plus their brand factory provides in less than 1000 excluding discounts, with discounts and rewards points and other benefits like cashbacks it makes customers more keen to buy and purchase more. So, the Future Brand was looking very attractive and that’s when I brought the stock of FUTURE LIFESTYLE.

In 2018 I purchased shares of FUTURE LIFESTYLE at a price of 69.54 which went up till Rs 482.30 and we are expecting a price rise till Rs 1200- 1500.

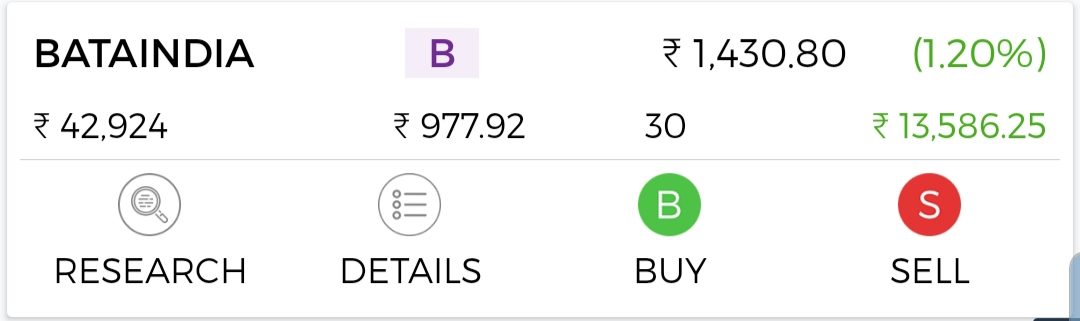

BATA INDIA:

How much pairs of shoe do you buy in a year? Probably not more than 2 pairs in average within a span of 5 years. If you go through a survey in your locality , you will find a limit of 1 pair within average people because most of them are not accustomed to buy shoes within 1–2 years. Till yet, so many villagers do not use shoe or use rarely. Most of the middle income group of people are satisfied with cheap- priced shoes of local made having no such brand name. On the other hand, shoes are limited for self use only, no one buy it for gifting or any other purpose like textile or jewellery items.

Generally sale of shoes is increasing gradually from September to December. Duration of this 4 months is composed of festival monsoon through out different parts of our country. With this effect, investors are interested to buy stocks BATA INDIA, at low rate from June-July and try to book profit within next January. Reputed shoe companies are with positive business during this 4 months. For long term benefit, I think, this type of stock will not be So appreciable.

BATA INDIA is no doubt a pioneer reputed company but is not running with monopoly concept. Some other reputed companies are also ready to take vital part in advancement of business.

Considering all above factors, it is better to hold this stock for short term profit. At present. You may wait for it’s down turn level or to buy now and accumulate at low. Present fundamental may help it to touch rs 1000 any time within 2 months, which it actually did.

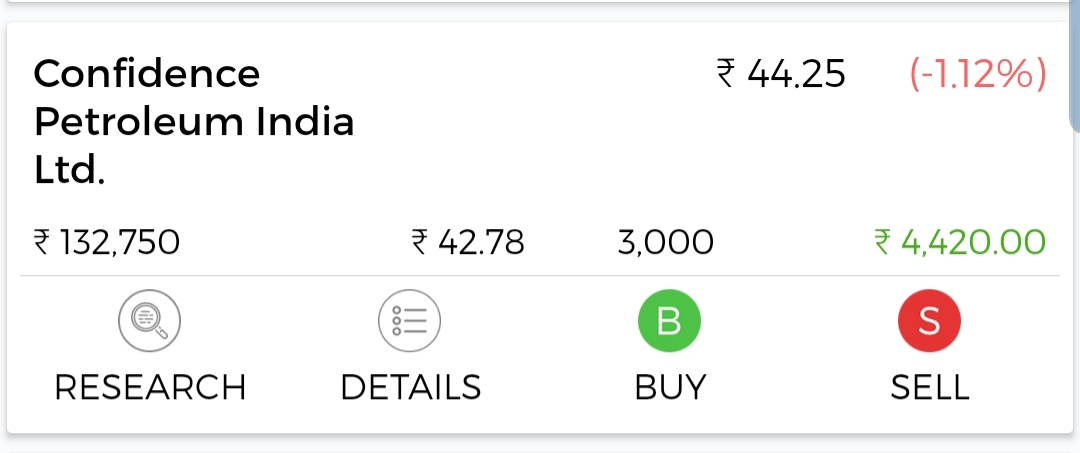

CONFIDENCE PETROLEUM:

It would be wise to enter the Petroleum Industry now. Petroleum demand is expect to rise from 4.5–5 Million bpd to 10 million bpd in coming two decades. Confidence petroleum is a relatively smaller company with tremendous scope in the near future.

Coming to its products, they have captured the most important sector. Auto LPG, it has been the most preferred vehicle fuel because of its environment-friendly nature. Further, the height of CNG cylinders is almost 3x higher than LPG cylinders. It is more expensive to transport CNG across the country because of its gaseous state (requires pipelines or heavily reinforced tankers) whereas LPG can be easily transported to any corner of the country because of its liquid state (using lighter height tankers). Moreover initiatives taken by the southern states for greener fuel to be used for all public transport. This will considerably increase the demand for new LPG Pumps across the country.

The company has started 30 new LPG Pumps in the last year. The Company is planning to set up 60 – 80 new LPG pumps during the course of the current financial year. They have a target to reach 200 to 220 pumps by FY 2018-19 They are also taking diligent steps to improve the performance of inefficient and low-performing stations. During the year, the Company relocated around 10 stations with low operations to higher volumes area. Further, the Company has set up a program to convert petrol-run Auto rickshaws into LPG-run ones, which will support its overall volume growth strategy besides helping in reducing pollution. The Company has 58 LPG Bottling plants and 4 Blending plants across 22 states, and it plans to add another 16 LPG Bottling plants in FY 2018-19 & FY 2019-20. It aims to set up around 100 LPG Bottling plants over the next three years for its own use and for providing filling assistance to PSU Oil Companies. These bottling plants fulfill two key aspects or our business: one, they act as storage points for our Auto LPG pumps, where storage capacity is limited due to city restrictions. Two, they provide filling services for our packed cylinder division. Due to their logistic advantage and cost-efficiency, PSU oil companies prefer availing our LPG Bottling assistance, wherever they have such a plant.

The management expects 100-500% growth in this vertical in the next three years, which is possible due to our large scale of operations and strong dealer network (800 dealers pan India). They also expect strong growth in LPG bottling assistance revenues, due to forthcoming new tenders by PSU oil majors across India and due to demand created by successful implementation of The Pradhanmantri Gram Ujjwala Yojna.

Looking at the above points or rather upward growth strategies I would advice all the investors to hold the share for this company as it will have a hike in its price in near to short term.

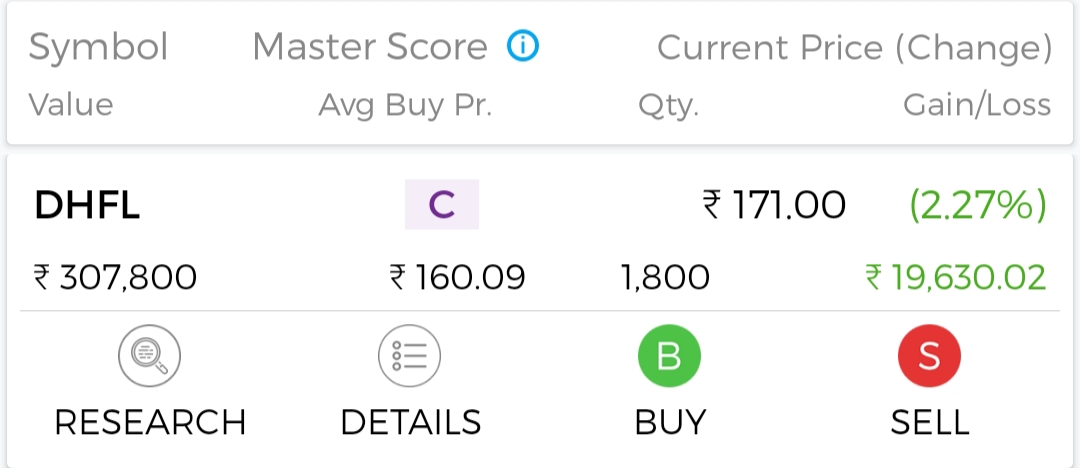

DHFL:

DHFL Ltd (Dewan Housing Finance Ltd) was established by Late Shri Rajesh Kumar Wadhawan in the year 1984. He wanted every Indian to own a home and this vision of his laid to incorporation of DHFL Ltd. Over 33 years have passed since the company’s inception and today DHFL stands strong as one of India’s leading housing finance companies. DHFL reaches the vast-customer base through network of 348 offices spread across the country.As a group, product offerings also include insurance, mutual funds, education loans etc. by way of various associate and subsidiary companies. Strong Management team has played a major role in success of the company. It is expected to strengthen in future.

DHFL having a book value of Rs331(approx) and current price 237(approx). Analysts believe that a stock trades below it book value then the stock is very likely to stabilize near its book value. In the long run various rumors didn’t even effect the company instead had a growth of 21.45% in the 5years. Coming to its management DHFL has a strong management and organization which actually has lead this company to a higher ground. Deeper distribution of its service in both rural and urban area with its efficient and effective service to all classed people is highly been appreciated. Lately, DHFL has been facing some serious competition pressure leading to deflation of its growth but despite that it is still holding its position which explains that the company has got strong pillars to hold on. Further, sustained demand backed by ever evolving and well defined RBI and NHB guidelines has kept the sector low risk, therefore attracting many players that can contribute the sector.

Housing finance sector has sweet spot so far. So with this encouraging background people already invested should hold this share in the future for it will have a serious hike in its price proving as a muiltibagger.

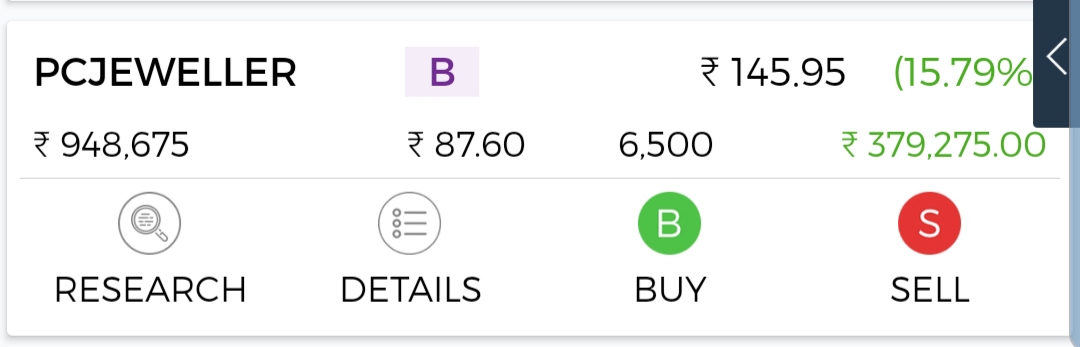

PC CHANDRA JEWELER:

It was started in 2005 with one store in Karol Bagh, Delhi. Since, it has spread widely across the country and is very prominent in North India.

Now what made this company rise up is what I am going to tell you. Opening with, a recent announcement made that PC Jewellers will reduce its financial cost by not considering the buyback of shares and repaying the debts that they have taken.

This indicates a good management strategy for the company.

Like this, there might be many other decisions that the company might have taken or will take in the future. As a prudent investor, a proper analysis needs to be done before buying or selling the stock. The first and most important aspect of PCJ is that it focuses on the organised jewellery market.

It sets up large format standalone showrooms at high street locations, where it stocks a wide range of jewellery across all price points. The main focus is on diamond jewellery. It sells only hallmarked and certified diamond jewellery which has helped it gain trust among its customers and build its brand name.

If one looks at its financial statements over past 5-7 years, we can find that it was in the mode of rapid expansion for building the retail chain of stores. This has led to an increase in its overhead costs. At the same time, it has been successful in generating revenues to keep on consistently increasing its top line and bottom line.

A few parameters that prove this are its sales grew by 17% YoY basis, EBITDA grew by 9% YoY whereas PAT grew by 4% YoY. Export sales were also up by 10% and Gross margins improved to 14.4%.

Just expanding and opening stores in cities does not help one gain tremendous success. The company ties up with local designers in each location in addition to getting jewellery manufactured at its central manufacturing unit in Delhi.

In 2013 PC Chandra Jewellers ventured into south India in Mangalore, Bengaluru, and Hyderabad (50% of the inventory of this market is localised due to the preference of local designs). Till 2015 its focus was to expand domestically and export sales mainly focused on NRIs looking for Indian handmade jewellery.

One of the surveys also pointed out that PC Jewellers had lower making charges as compared to other jewellery brands. This was owing to their designers chose. Also, the strategy adopted to locate the manufacturing plant helped reduce 2-3% in making charges.

Roping in various film stars like Akshay Kumar, Twinkle Khanna, Shilpa Shetty, Bipasha Basu, Vidya Balan, etc. has helped PCJ a lot too.

These are few of the reasons that stock price was very high of PC Chandra Jewelers. All those factors mentioned above have contributed to this consistent rise in fame and led to the success of PC Jewellers.

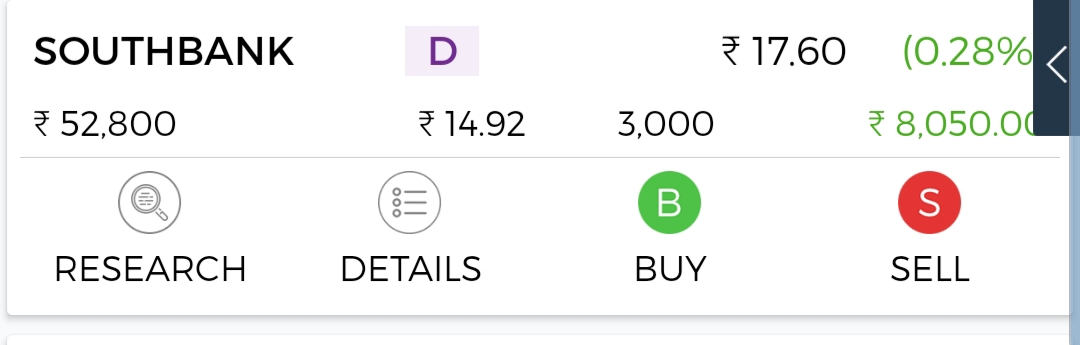

SOUTH INDIAN BANK:

One of the earliest banks in South India, “South Indian Bank” came into being during the Swadeshi movement. The establishment of the bank was the fulfilment of the dreams of a group of enterprising men who joined together at Thrissur, to provide for the people a safe, efficient and service oriented repository of savings of the community on one hand and to free the business community from the clutches of greedy money lenders on the other by providing need based credit at reasonable rates of interest. Translating the vision of the founding fathers as its corporate mission, the bank has during its long sojourn been able to project itself as a vibrant, fast growing, service oriented and trend setting financial intermediary.

Coming to the company, the strength are its pillars to grow in present and even in near future. You see, the growth progress expectations are rather promising. Indeed, sales are expected to rise sharply in the coming years. The group’s activity appears highly profitable thanks to its outperforming net margins. The equity is one of the most attractive in the market with regard to earnings multiple-based valuation. The company is one of the best yield companies with high dividend expectations. Over the last twelve months, the sales forecast has been frequently revised upwards. And to be honest all the Analysts have a positive opinion on this stock. Average consensus recommends overweighting or purchasing the stock. SOUTHBANK currently trades below 200 weeks moving average by 5% and 200 weeks moving average is more than 100 weeks moving average. Once it crosses and closes above 22.95 on weekly basis, it will catch buying momentum and we can expect 229.50 in 5 to 10 years time frame. Moreover South Indian Bank, with a price-to-earnings (P/E) ratio of 12.67x, always catch the eye of investors on the hunt for a bargain. It tells us that SOUTHBANK is undervalued relative to the current IN market average of 22.04x , and undervalued based on its latest annual earnings update compared to the banks average of 21.82x .

So basically an undervalued stock with such attractive strengths will obviously provide returns an investor expects.

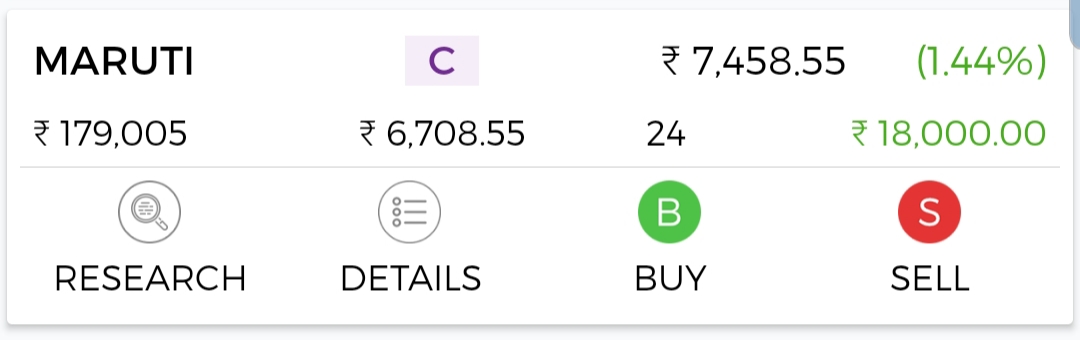

MARUTI:

Maruti Suzuki India Limited, formerly known as Maruti Udyog Limited, is an automobile manufacturer in India. It is a 56.21% owned subsidiary of the Japanese car and motorcycle manufacturer Suzuki Motor Corporation. As of July 2018, it had a market share of 53% of the Indian passenger car market. Maruti Suzuki manufactures and sells popular cars such as the Ciaz, Ertiga, Wagon R, Alto K10, Swift, Celerio, Swift Dzire, Baleno and Baleno RS, Omni, Alto 800, Eeco, Ignis, S-Cross. The company is headquartered at New Delhi. In May 2015, the company produced its fifteen millionth vehicle in India, a Swift Dzire.

Now coming to its strengthened pillar, Total no of passenger vehicles(PV’s) sold in FY18 by MARUTI was about 1.77 million units as against 1.56 million units in FY17.Domestic sales of the company was 1.65 million units in FY18 as against 1.44 million units in FY17. MARUTI has close to 53% market share in PV’s (which was about 47% in FY17 )so there is a jump of close to 6% in the company’s market share and it is closely inching towards 55% mark. Company’s models are showing sales growth across the board, be it alto, wagon r in mini car segment or swift , baleno in compact car segment or s cross, brezza, ertiga in utility car segment. The PV segment in INDIA as a whole is expected to grow at about 8.5 /9% year on year which is a very healthy growth and a company with more than half of the industry’s share is a sure shot beneficiary. Moreover, as an Indian, in selecting a car the first company that comes into ones mind is MARUTI because of its low maintenance and high resale value which lack in its competitors (thats why they are losing market share) and thus it has a strong foothold in the rural market too.

For me reasons are quite strong to invest in MARUTI’s stock for all the reasons above gives a clear idea that the stocks of this company are going to get a hike in the near future.

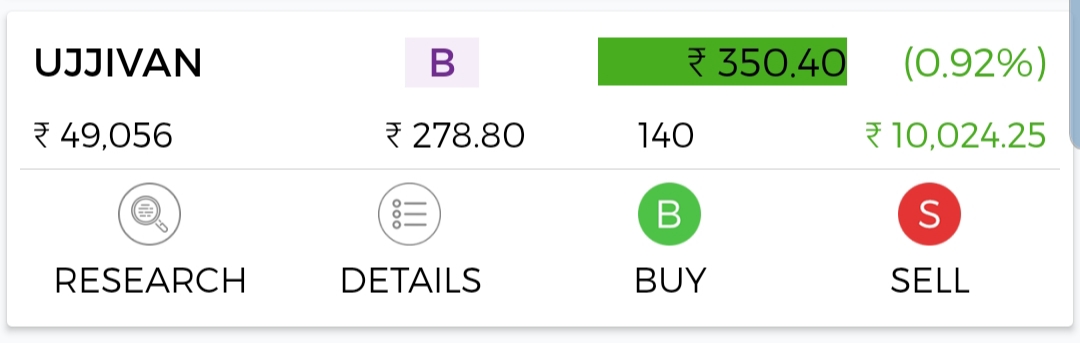

UJJIVAN:

Ujjivan Financial Services Limited started operations as a NBFC in 2005. On 7 October 2015, Ujjivan received an in-principle approval from the Reserve Bank of India to set up a small finance bank. At the time, the company already serviced over 2.6 million customers from 464 branches in 24 states. The small finance bank status provided the opportunity to expand Ujjivan’s range of loan products, and also to accept deposits rather than relying on other financial institutions to provide funds for the loans. Ujjivan received the final license from the Reserve Bank of India on 11 November 2016 to set up a small finance bank. Ujjivan is present across 24 states and union territories, and 209 districts in India, catering to over 3.7 million customers.

Now, people might ask why UJJIVAN FINANCIAL SERVICE?

You see, the opportunity size is massive and companies can increase loan book 4-5x in the next 5 years.With newly acquired license of Small finance bank the political risk has decreased substantially.Net NPA of 2 Cr. on AUM of 4080 Cr. lower than peers. Large Banks Not interested in providing loans of INR 15000-20000 as collecting cash from small borrowers it’s too tedious for the big banks.

We believe that Ujjivan can grow at 30% plus rates for long periods of time. There are always risks in fast growing companies, though the biggest risk in Microfinance stems from political risk. Moreover, Ujjivan is priced lower than its peers Equitas and SKS microfinance. We love companies that are growing fast, ethical management and we can buy them a reasonable price. We intend to hold this stock for the next 2-3 years and compound money for our clients at higher rates.

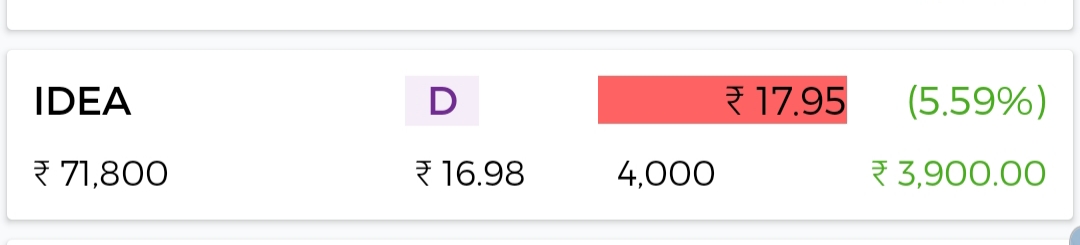

IDEA:

We all know that the Idea and Vodafone are merged now and it’s no more Idea Cellular but Vodafone Idea. Okay that’s good, sounds good two companies got merged but what is the benefit you can make out of it? Not being a user but an Investor! Well, we know about Idea first in detail so that we can understand it much better what we can expect out of it.

The merger of Idea and Vodafone India got completed. The leadership team of Vodafone Idea Ltd. has already been announced on March 22, 2018 and the new management was ready with an extensive plan to consolidate the operations and network of the two companies in a phased manner.The key focus area for the merged team is be to fast forward the substantial cost synergies with an estimated NPV of ~$10bn and rapidly expand the broadband coverage and capacity by redeployment of overlapping equipment & refarming /consolidation of spectrum etc.

The combined entity named ‘Vodafone Idea Ltd.’ will be India’s largest mobile operator and the 2nd largest in the world, with nearly 408 million subscribers.

Both the companies had set up respective project management teams, preparing for the merger and initiated detailed planning long back. Both the companies now, under ‘Active infrastructure sharing’ programme and ‘2G and 4G ICR arrangements’ across various service areas, share around 49,000 sites. Planned Fibre and PoP sharing programme is also underway in Top 220 cities across the 22 telecom service areas.

Telecom infrastructure firm Bharti Infratel made a statement that its consolidated revenue, including that from Indus Towers, is expected to take around Rs 780 crore hit on annual basis, due to exit of Vodafone and Idea Cellular from co-located mobile

Bharti Infratel and Vodafone own around 42 per cent stake each in Indus Towers and rest of the stake is held by Aditya Birla group firm Idea Cellular.

Vodafone and Idea have merged their mobile businesses and now they are in process of consolidating assets to trim operational and capital expenses.

In order to this, we can see NSE: IDEA a good stock to bet on for a long term future. It may not be a wonder to see IDEA at a level of 204 again soon which was there in year 2015.

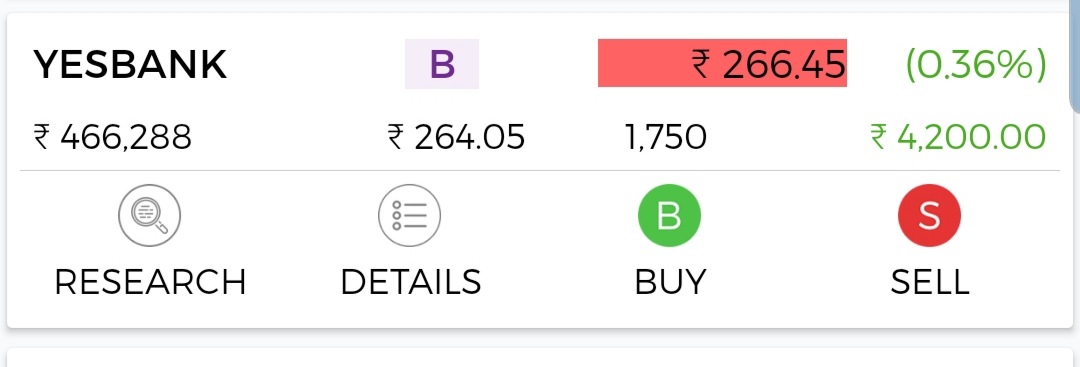

YES BANK:

Yes Bank Limited is India’s fourth largest private sector bank, founded by Rana Kapoor and Ashok Kapur in 2004.[4] It primarily operates as a corporate bank, with retail banking and asset management as subsidiary functions.

Being the fourth largest private sector bank The company primarily serves customers in the food and agri business, life sciences, healthcare, biotechnology, telecommunications, etc. The bank has maintained a healthy asset quality profile and has more than doubled its branch network over the past 18 months. Its capital adequacy ratio, which determines the bank’s capacity to meet time liabilities and other risks, continued to be strong at 16.1%. The tier-I core capital, which includes equity capital and disclosed reserves and is the measure of a bank’s financial strength, stood at 9.2% The net profit of the company grew 32.9% on a year-on-year (YoY) basis to 254 crore driven by healthy growth in operating income and lower-than-expected provisioning expenses. Advances grew by 15.3% on a YoY basis, while deposits grew by 19.5% during the same period. YES Bank had aggressively hiked the savings account interest rate immediately after it was de-regulated, which helped in strengthening the weak link in its liability franchise. As the bank is primarily wholesale-funded, it is likely to benefit from any trend reversal in the interest rates. The soundness of the pricing power is proven by the fact that of the 58 analysts tracking the stock, 51 recommend a ‘buy’ rating. Rural Electrification Corporation The company is engaged in the financing and promotion of transmission, distribution and generation projects in India. It has an immense growth potential due to its higher business visibility and stable margins In the third quarter of 2011-12, it posted a net interest income of `10.1 billion, up 19% on a YoY basis, while profit after tax was up 24% on a quarter-on-quarter (QoQ) basis at `7.7 billion. The loan book grew 24% during the same period and 5.1% on a QoQ basis to `950 billion.

Quite a promising background and eye catching to all the investors and that is the reason why I myself invested in this particular stock. And to be honest this share has a lot more potential in the near future and can provide a huge return. So people already holding the shares should hold for some more time.